PCOS to PMOS | Here’s What You Need to Know

In this post I will go over everything from what PCOS + PMOS mean, to PCOS symptoms, to effective and holistic PCOS treatment. But the thing I want you to hold onto right now is that this new metabolic perspective on PCOS is not new information. And more importantly, the rename from PCOS to PMOS does not mean your medical providers instantly know how to address the root causes of your PCOS symptoms.

I’ve been helping females with PCOS symptoms by addressing their gut health, metabolic health, and endocrine health, for as long as I’ve been in practice - including my own PCOS!

I’ve Been Saying it for Years…

Your PCOS diagnosis has been rightfully renamed to PMOS - a win for female-bodied folx everywhere!

In this post I will go over everything from what PCOS + PMOS mean, to PCOS symptoms, to effective and holistic PCOS treatment. But the thing I want you to hold onto right now is that this new metabolic perspective on PCOS is not new information. And more importantly, the rename from PCOS to PMOS does not mean your medical providers instantly know how to address the root causes of your PCOS symptoms.

I’ve been helping females with PCOS symptoms by addressing their gut health, metabolic health, and endocrine health, for as long as I’ve been in practice - including my own PCOS!

Hello, my muffin tops. I’m Hilary Beckwith, ex-dieter and functional health expert. Women with PCOS/PMOS, IBS, and autoimmune conditions come to see me with signs of adrenal stress, insulin resistance, and inflammatory conditions, and my job is to find the root causes so we can address their symptoms more effectively and fill in the gaps between their lab values and how their body actually feels. Before you continue, click here to read my Medical Disclaimer.

In this article, you’ll learn:

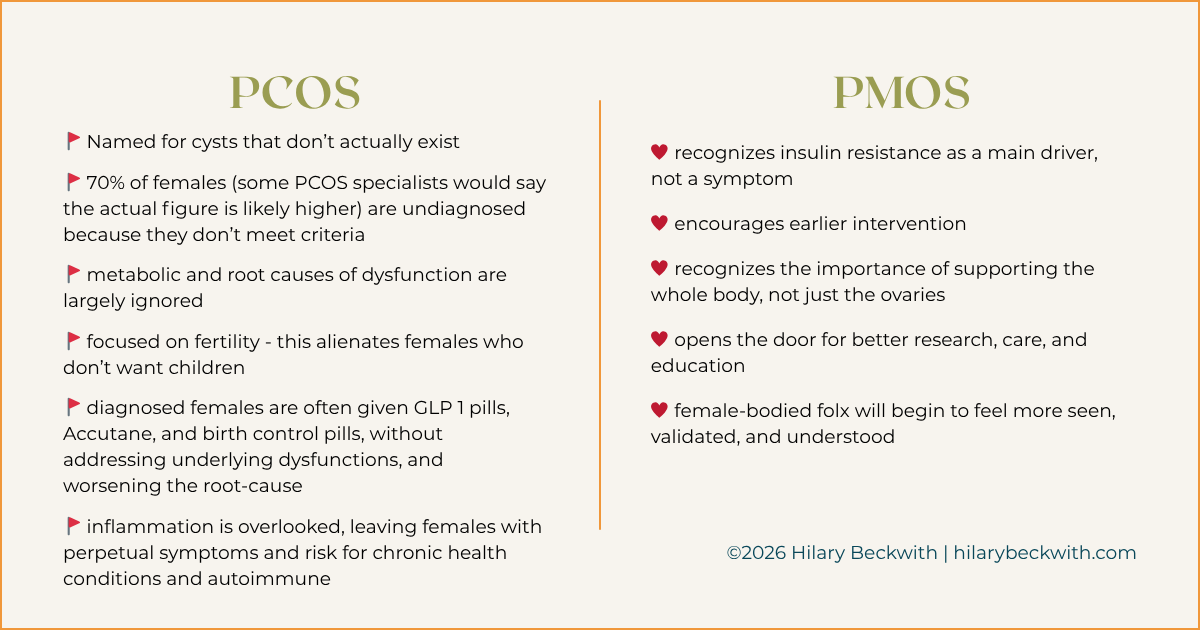

Differences between PCOS diagnosis and PMOS

Why the rename is so important

PCOS treatment with functional nutrition

Ways you can start advocating for your health in more meaningful ways

the name PCOS has always been a problem

And this is a huge disservice to female-bodied folx everywhere. When I got my PCOS diagnosis nearly 20 years ago, I was told, “you will probably become diabetic” and that I would not be able to get pregnant without expensive medical intervention. That was the only guidance I received from my gynecologist.

I didn’t know then how to advocate for my health, ask questions, or seek out a second opinion, or even holistic support. But I know now, and that’s why my ongoing mission is to educate and empower a new generation of women to do the same by holding their practitioners accountable, asking questions, and getting heard, no matter what it takes.

The first step is to educate yourself.

WHAT DOES PCOS STAND FOR?

PCOS stands for PolyCystic Ovarian Syndrome. Getting a PCOS diagnosis primarily requires a female to meet at least two of these measures:

elevated androgen levels

irregular or absent ovulation

an ultrasound confirming multiple “cysts” on the ovaries

more recently, low egg count was added to this list

You can see, these criteria largely point to a gynecological focus - here’s why that’s a problem:

Elevated androgens and sex hormone imbalances don’t just happen. In general, are often caused by a disruption in the HPA axis (brain and adrenal glands), blood sugar instability (also tied to HPA axis), prolonged chronic stress (oh hey, that’s HPA axis, too!), and liver functionality.

Ovulation issues stem from these same hormonal imbalances, caused largely by - yep! - HPA axis dysfunction and blood sugar instability or insulin resistance. While it’s true that the ovaries themselves can contribute to the problem, the root cause is often in communication between the brain and ovaries, not the ovaries themselves. Chronic stress, insulin resistance, and liver health can all be supported to improve ovarian function.

PCOS ovaries are not covered in “cysts”: The classic visual of PCOS is this picture of an ovary covered in what looks like a string of pearls - these are not cysts - they are follicles that were not able to release an egg into the fallopian tube, and thus became stuck. Your ovaries can develop cysts, but what is seen in PCOS is not cysts.

What’s more, the cause of these stunted follicles is commonly caused by an increase in androgens (testosterone, DHEA) produced by the ovaries in response to elevated insulin levels, caused by insulin resistance - again, not a gynecological issue.

Egg Count: The quality of eggs is vastly more important than the number of eggs. Think about it - does it do you any good to have a drawer full of dead batteries, if only 2-3 of them have any juice left?

WHAT DOES PMOS STAND FOR?

PMOS stands for Polyendocrine Metabolic Ovarian Syndrome. Polyendocrine, meaning it involves many factors in the endocrine system, including metabolic, or blood-sugar-regulating endocrine glands such as the adrenal glands and pancreas.

Take a close look at the diagram below to see the differences between a PCOS diagnosis and PMOS.

renaming PCOS to PMOS does not mean your doctors instantly know how to support you

Whether we call it PCOS, PMOS, or the acne-bloat-crazy-bananas-plague - PCOS is a complex interplay of dysfunction in metabolic health, hormones, liver, gut, and brain.

The renaming of PCOS to PMOS is a step in the right direction, but the medical community still has a long way to go when it comes to understanding how to treat PMOS effectively. This rename will bring more awareness to the medical community, leading to better research and education for medical providers, but that is YEARS down the road.

After all, it took decades before medical doctors even started to become aware (awareness does not equate to action) that more nutrition education would be helpful to their patients. The minuscule amount currently required for medical licensing is largely focused on biochemistry, not patient care.

And while it would be a dream come true to find that one-stop shop for full-body PCOS and PMOS treatment, it simply does not exist, and probably won’t for some time.

That’s why practitioners like me exist - I am in practice to help female-bodied folx uncover hidden causes of their dysfunction that are keeping them stuck in their PCOS symptoms.

Through a focus on gut health, digestion, inflammation, stress, and blood sugar stability, I have helped my female-bodied clients (myself included) break free from PCOS symptoms such as:

painful and embarrassing adult acne

“PCOS belly” - weight in the belly and hips that came out of nowhere

thinning hair

irregular and unpredictable periods

PMS or PMDD (despite what you might have learned, PMS is a sign of hormone imbalances, and is not normal to experience)

hormone imbalances reflected on labs

fatigue + energy crashes

2am wake-ups

increased body or facial hair (hirsutism)

“hangry” between meals

poor mood - feeling unstable, depressed, or anxious

whole-body PCOS treatment

Most females who seek my help present with some form of hormonal imbalance, signs of prolonged chronic stress, and systemic inflammation. So, PCOS diagnosis or not, the main goal is to assess and pinpoint what the root causes of dysfunction are, so that we can create a care plan that is targeted to their specific needs.

After years of throwing spaghetti at the wall, the women who work with me walk away feeling seen, heard, and revitalized - a stark contrast from the providers’ offices that, in the past, left them feeling dismissed, ignored, and alone.

TARGETED, WHOLE-BODY PCOS TREATMENT THAT GETS RESULTS:

LIFESTYLE + DIETARY ANALYSIS:

I’m not interested in how many calories you eat per day, nor will I ever ask you to step on a scale. However, day-to-day stress levels, food quality, meal timing and atmosphere, sleep, bowel movements, body movements - all of it matters.

Chronic stress disrupts the brain’s communication with endocrine glands. This is because your brain’s priority in stress response is protection - or better yet, survival. Nothing else is important until that threat (stress) is successfully dealt with. And when the stress keeps coming, you stay stuck in survival mode, and this plays havoc on your hormones. The first thing I do is gather information so that I can meet you where you’re at.

ASSESS DIGESTIVE HEALTH:

This is a big one with PCOS. Digestive dysfunction is more than just gassy evenings, heartburn, and constipation. When your body does not produce enough stomach acid, digestive enzymes, or cannot efficiently move food through your intestines and eliminate waste - intestinal tissues become damaged and inflamed, toxic burden builds due to waste that is not eliminated, and your susceptibility to opportunistic bacterial overgrowth, candida, and even parasites, increases significantly.

Your digestive system is wired to kill off harmful pathogens and prevent their proliferation - and the biggest inhibitor of digestion is stress.

FUNCTIONAL LAB TESTING:

For cycling females, getting a one-time blood panel is not enough information to understand the big picture, and quite frankly, if you are a cycling female, it is a huge disservice to use hormone levels on a single blood panel as a starting point. Chances are that provider is simply just ticking off the boxes required by insurance to diagnose you (Click HERE to learn more about how this impacts your access to quality health care).

Working with quality functional labs, we can create a plan that is fine-tuned to your body’s specific needs, as opposed to suppressing symptoms alone. Here are the labs I most commonly recommend with PCOS symptoms:

GI-MAP (Diagnostic Solutions) - measures microbial balance, pathogens, inflammatory markers, and digestive markers.

Organic Acids Test (Mosaic) - measures for yeast and mold, neurotransmitter dysfunction, mitochondrial health, and nutrient deficiencies.

Expanded Female Hormone Panel (eFHP - Diagnostechs) - Spanning across your entire cycle, this test measures FSH, LH, Estrogen, Progesterone, Testosterone, and DHEA, and helps us locate patterns and sources of dysfunction (e.g. is the source of the problem brain-ovary communication, or is it in the gland itself?)

DUTCH Adrenal (Precision Analytics) - Measures daily cortisol rhythms, DHEA-S, and your body’s cortisol clearance and detoxification ability.

DUTCH Complete (Precision Analytics) - Measures multiple reproductive hormones as well as their metabolites and your body’s ability to detoxify each of them. It does not measure FSH or LH but is a powerhouse of information for males and females alike.

You can see that the focus with functional nutrition is not calories, diet, or weight loss - or even the lab values themselves - the focus is function.

Uncovering the root causes of dysfunction that are keeping you stuck in your inflammatory state, your constant bloat and discomfort, your debilitating fatigue, sugar cravings, and overall well-being.

ways to advocate for your own health right now

The PCOS-to-PMOS change only happened recently. It is highly unlikely that you will walk into your OBGYN tomorrow and get whole-body, root-cause support for your PCOS diagnosis. It may take years or even decades for medical providers to start receiving training that will help you the most.

The medical system trains doctors to know what to do when your health fails. It’s not their fault, but “conventional” medicine does very little to help connect your symptoms to your data.

You are among a generation of cycle-breakers, friend. The ripples have to start somewhere - let it be with you!

HERE ARE SOME WAYS TO START ADVOCATING FOR YOUR HEALTH STARTING TODAY:

Stop waiting until self-care “fits”: Now is when your body needs help. And now is when you’re worthy enough to receive it.

Stay curious. Your healthcare providers, including me, are humans just like you. We each have our own set of knowledge, skills, and biases that influence how we show up in the world and with our patients/clients. HEALTHCARE PRACTITIONERS ARE NOT ALWAYS RIGHT. Ask questions and don’t believe everything you hear (including from me!). Ask for evidence and make your own interpretations.

Stop scrolling TikTok. Stop falling for bio-hacks, supplement packs, expensive wearables, and cleanses that were not recommended based on a personalized assessment of your body’s needs.

Talking is free. Leave comments below or email me with your questions. I love connecting with health-curious folx.

was this helpful?

Leave your questions and comments below, and if you are finally ready to start addressing your PCOS symptoms at the root, now is the time!

Click the button below to get started for free.

Food Sensitivity Testing and Parasites | The Missing Piece

Having food allergies does not mean you have parasites, just as having parasites doesn’t necessarily mean you will develop food allergies.

But when working with 1:1 clients, and I see food (or seasonal) allergies that developed later in life, that is information worth digging into.

The Missing Piece in Your Food Sensitivity Test

Food allergy testing and food sensitivity testing have been all the rage in the past few years in the holistic health world. I get more into the differences (and they’re big) between food allergies and food sensitivities in a recent post. But in this article, I want to talk about an important, and often overlooked, hidden cause of food allergies that your practitioner may be overlooking: parasites.

Hi lovelies. I’m Hilary Beckwith, ex-dieter and functional health expert. Women with PCOS, IBS, and autoimmune conditions come to see me with signs of adrenal stress, insulin resistance, and inflammatory conditions, and my job is to find the root causes so we can address their symptoms more effectively and fill in the gaps between their lab values and how their body actually feels. Before you continue, click here to read my Medical Disclaimer.

In this article, you’ll learn:

how your body responds to food allergies

how your body responds to parasites

how to find and address parasites

is your food allergy actually a food sensitivity?

Some use the terms food allergy and food sensitivity interchangeably, and here’s why it’s important to know the difference. They’re two different types of responses by the immune system that require two different types of testing.

If you go to your doc and tell them you think you have food allergies, they’re going to run a food allergy test, which will provide negative results if you actually have a food sensitivity.

Let’s explore the differences in the diagram below:

your body’s response to parasites

The most relevant takeaway from the above table is that food allergies involve IgE antibodies. In fact, most allergies, not just food, involve an IgE response.

What does that have to do with parasites?

Studies have shown that IgE levels increase with parasite presence in humans. Not all parasites - but most.

This is meant to be a protective mechanism against the parasite; however, the increase in IgE levels in the body increases susceptibility to having an allergic reaction to foods. Although more research is needed, the current thought is that proteins from foods that are structurally similar to certain parasites are attaching to IgE antibodies and activating an allergic response.

It’s why when I meet a client who has developed food allergies later in life, and somewhat suddenly, my first suspicion is parasites.

HERE’S HOW IGE ANTIBODIES WORK

IgE antibodies develop as a defense against an allergen - an antigen that causes an allergic response.

These Y-shaped antibodies attach themselves to mast cells - cells that primarily line mucosal tissues, such as lungs, intestines, sinuses, under the skin, etc. - and wait for an allergen to show up.

When said allergen arrives, it attaches to one or more IgE receptor points(the two points at the top of the Y). When two IgE receptors have been activated, this triggers mast cell degranulation - meaning, the cell opens up and releases a surge of toxic, inflammatory substances that damage surrounding cells and molecules, including the allergen.

This is a great video description for all you visual learners.

do you need a parasite cleanse?

Having food allergies does not mean you have parasites, just as having parasites doesn’t necessarily mean you will develop food allergies.

But when working with 1:1 clients, and I see food (or seasonal) allergies that developed later in life, that is information worth digging into.

Parasites are sneaky. They are really good at evading lab testing and the immune system, due to their ability to signal “everything is fine - nothing to see here” to the immune system. In fact, there is ongoing research into the effects of a specific few parasite types that might actually have a protective impact on those with autoimmune conditions.

Personally, I scored very low on the very same screening questionnaire I offer clients, and I lab-tested negative (twice) - yet I still found parasites when doing a cleanse.

We need a clearer picture of overall health to know whether a parasite cleanse is right for you. Here are some things I consider when assessing a client for parasites:

digestive health

inflammation markers on lab testing

immune markers on lab testing

parasite symptoms

potential parasite exposures (swimming in standing water, consuming raw or undercooked meats and fish, allowing pets on furniture, pets licking your face, frequent interactions with children, etc.)

before you rush into a parasite cleanse

Parasite cleanses are a trendy topic right now, and that means there is a huge influx of influencers (and some practitioners) wanting to sell you parasite eradication products you may not need. Many of these influencers and practitioners do not have proper training to assess for and address parasite infections - but I do.

As a Restorative Health Practitioner, I have been trained in parasite eradication and have even experienced success with it myself.

Parasite eradication is not a one-and-done event. Parasite cleanses are a whole-body problem and require:

healing and repair to tissues damaged by parasites

functional support to address the digestive mechanisms that, if working optimally, should prevent you from getting a parasite infection in the first place

a knowledge of the parasite’s life cycle - many parasite cleanses only address mature parasites, not their eggs or larvae

the ability to adjust supplements and methods according to your body’s response to the process

Before you jump into some expensive product line from someone who happens to be really good at talking, consider getting a more functional perspective to help you reduce food allergies, lower inflammation, and repair the mechanisms that are meant to protect you from parasite infections.

A parasite symptom checker is available to clients completing an initial assessment. Click the blue button below to help us get to know each other first.

Want to keep reading? Click HERE to read my parasite story.

Why Your Health Insurance Plan Won’t Cover Functional Nutrition

One thing is common for us all - we are wildly in the dark about how health insurance works and who decides what’s covered. That is why my intention with this article is to offer clarity and education, so you can stop blindly allowing your health insurance plan choose your providers for you, and make more informed health decisions for yourself.

Why Your Health Insurance Plan Won’t Cover Functional Nutrition

It’s no secret that the healthcare system in the U.S. is a bumbling sh*tshow. We’ve privatized health insurance plans since the 1920s, causing costs to soar, excluding important health services, and making plans effectively useless to those who are relatively healthy.

It’s a complex issue, and a highly controversial one. I’ve worked in healthcare for 20+ years, both on the clinical side, and the billing side. I can’t change our severely broken system on my own. But, one reader at a time, I can help individuals like you know how to advocate for your own health when seeking out health insurance plans and healthcare services.

Hi darlings. I’m Hilary Beckwith, ex-dieter and holistic nutrition expert. Clients come to see me with signs of adrenal stress and inflammatory conditions, and my job is to find the root causes so we can address their symptoms more effectively and fill in the gaps between what their doctor is saying and what their body is saying. Click here to read my Medical Disclaimer.

In this article, you’ll learn:

is health insurance necessary?

what it means to use an “in-network” provider

the difference between “covered” and “non-covered” services (it might not be what you think)

is health insurance necessary?

For about nine years in the early 2000s, I worked for a large chain grocery store. I wore many hats there, but one of my jobs was to help change price tags when a new ad started every Wednesday.

I and my crew would replace expired sales tags with their regular price, as well as replace regular-priced tags with the new sales tags.

Every sales tag also showed the product’s regular price, so you as the customer could see how much you were saving by getting it on sale.

Here’s where things get shady…

Very often, when a product would go on sale, the store would increase the regular price of that item so that it looked like you were saving more money. When the sale ended, the regular price went back to its normal market rate.

In other words, the regular price on a sale item was completely arbitrary - it was used as a marketing tool to show how much the customer would “save”. [insert barfing noise]

Here’s the thing… Your health insurance plan does the same thing.

I’ll talk more about that later in the post. But first, let’s explore whether a health insurance plan is even necessary to have.

holding space

I want to be clear - the realities that we all live in are so different. What I have to say in this article will not relate to everyone. We each have different values and different needs to consider when choosing healthcare services and utilizing health insurance plan benefits.

One thing is common for us all - we are wildly in the dark about how health insurance works and who decides what’s covered. That is why my intention with this article is to offer clarity and education, so you can stop blindly allowing your health insurance plan choose your providers for you, and make more informed health decisions for yourself.

It is not at all meant to suggest that no one benefits from using health insurance. Plenty of individuals rely on private, state, and federally funded insurance plans to provide treatment for chronic illness and other medical conditions, and I hope to present this article with some sensitivity to that.

Earlier this summer I had a pretty serious injury - I fell while rollerskating, fracturing my ankle in three places, dislocating the joint, and detaching a ligament.

It required a trip to the E.R., surgery to repair the damage, multiple sets of imaging (before and after surgery), physical therapy, etc..

As a functional nutrition practitioner, I often look to treatment options that are root-cause-focused, as opposed to symptoms-focused. An injury like this requires a different approach.

I leaned into Western medicine (mostly covered by my health insurance plan), but I also utilized my nutrition background to optimize my healing, support bone density, regulate inflammation, regulate my nervous system after a traumatic injury, and support detoxification from pain meds (all not covered by my insurance).

So, was it necessary to have a health insurance plan in this instance?

I would argue yes… sort of…

I’ve already put in thousands of dollars toward premiums over the four years I’ve had this health insurance plan. Was it worth it for peace of mind? That’s debatable. Many Americans are terrified that the cost of healthcare, even with insurance, will lead them to crippling debt. You can read about my research on this topic here.

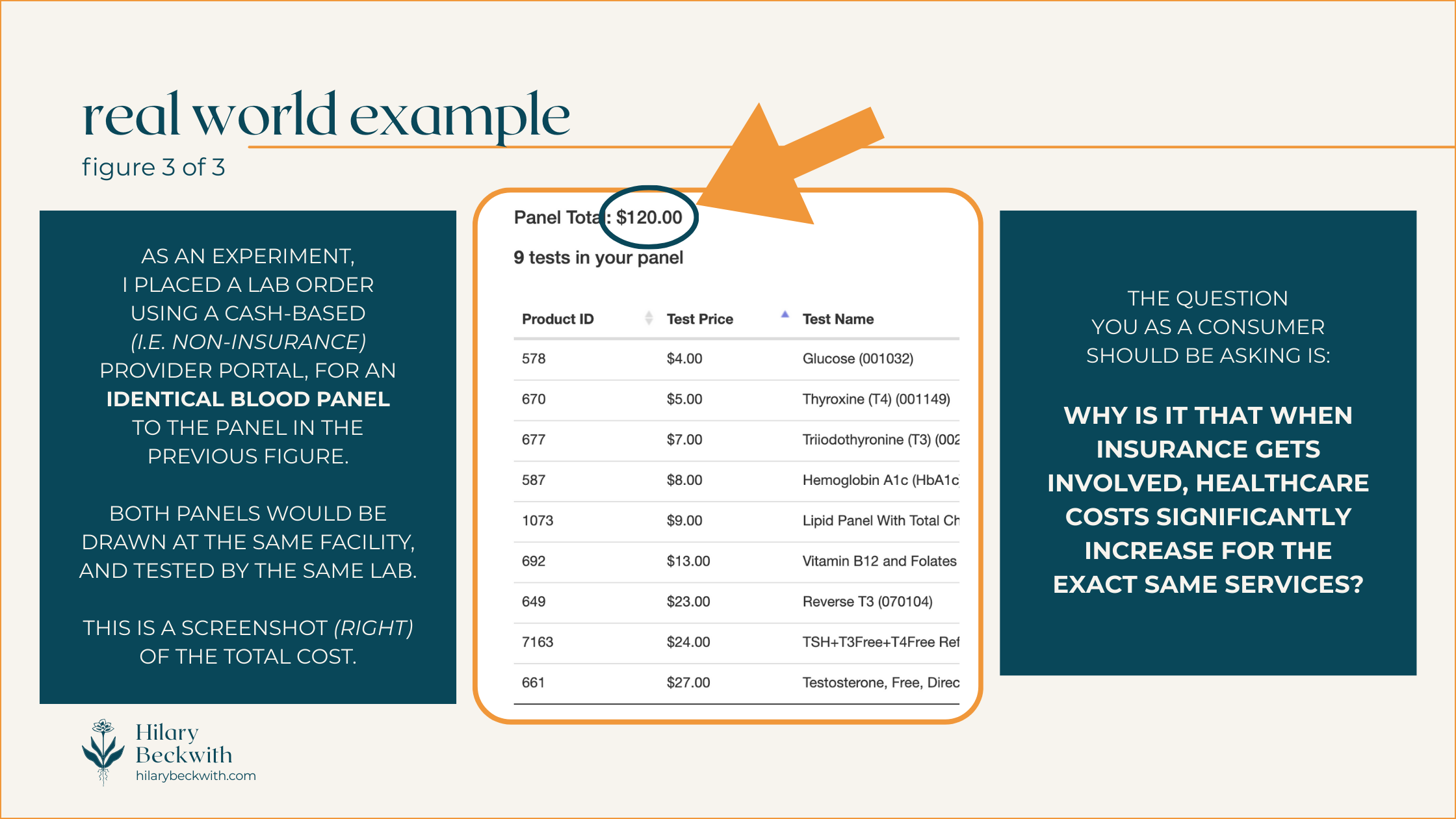

I certainly think there is a place for insurance, and an accident like this one is a good example of when insurance is necessary. But privatized insurance has been driving healthcare costs up (and up, and up…) since the 1920s [1], making quality healthcare largely inaccessible to many in the low or middle classes nearly 100 years later.

We’re all stuck between a rock and a hard place.

using an in-network provider

I think most of us understand that when using health insurance plan benefits, the question we most commonly ask a practitioner is, “do you take my insurance?”. After all, being in-network means the care will be cheaper, and in some cases is the difference between coverage or no coverage.

After working for nearly 25 years in medical clinics, I’ve learned that most people do not understand how their insurance works. And who can blame you!

SOME THINGS YOU MAY NOT KNOW ABOUT HEALTH INSURANCE:

INSURANCE IS A CONTRACT

The patient has a contract with their health insurance plan, as do any in-network practitioners. As with any contract, the terms look different for every health plan, but in general, the terms of patient-insurance contracts boil down to this:

IF the patient pays their portion, THEN insurance will pay theirs. Despite common belief, it is not the other way around.

PRACTITIONERS ARE NOT REQUIRED TO SUBMIT CLAIMS

It is not the responsibility of a practitioner to submit claims or pre-authorization requests on behalf of a patient. Practitioners typically take it on themselves simply because it’s easier for them to directly supply the information required by the insurance company, rather than have the patient be a liaison.

IT IS THE PATIENT’S RESPONSIBILITY TO UNDERSTAND THEIR OWN BENEFITS

Some practitioners are kind enough to give patients a cost estimate for care based on their insurance benefits - but it is not the practitioner’s responsibility to do so.

IT IS THE PATIENT’S RESPONSIBILITY TO APPEAL

Very often, health insurance plans deny services that should be covered according to the plan benefits (I recently experienced this, myself). In many of those cases, the practitioner is kind enough to submit an appeal on the patient’s behalf, again, because it is easier for the practitioner to directly submit required documentation. But it is not the practitioner’s responsibility to do so.

A PRACTITIONER WHO IS IN-NETWORK, TAKES A PAY CUT

If a practitioner is in-network with your health insurance plan, it means they have a provider-insurance contract with the insurance provider. That contract, in essence, says that in exchange for advertising (i.e. a directory, or network, of “preferred” practitioners), practitioners agree to discount their care, so that the insurance does not have to pay out as much.

Patients will often see these discounts conveyed as “you saved $___!” on their Explanation of Benefits (EOB).

IN-NETWORK PRACTITIONERS MAY BE LESS LIKELY TO SEEK OUT ROOT CAUSES OF YOUR SYMPTOMS

When practitioners are contracted with an insurance plan, they are subject to the regulations of that plan.

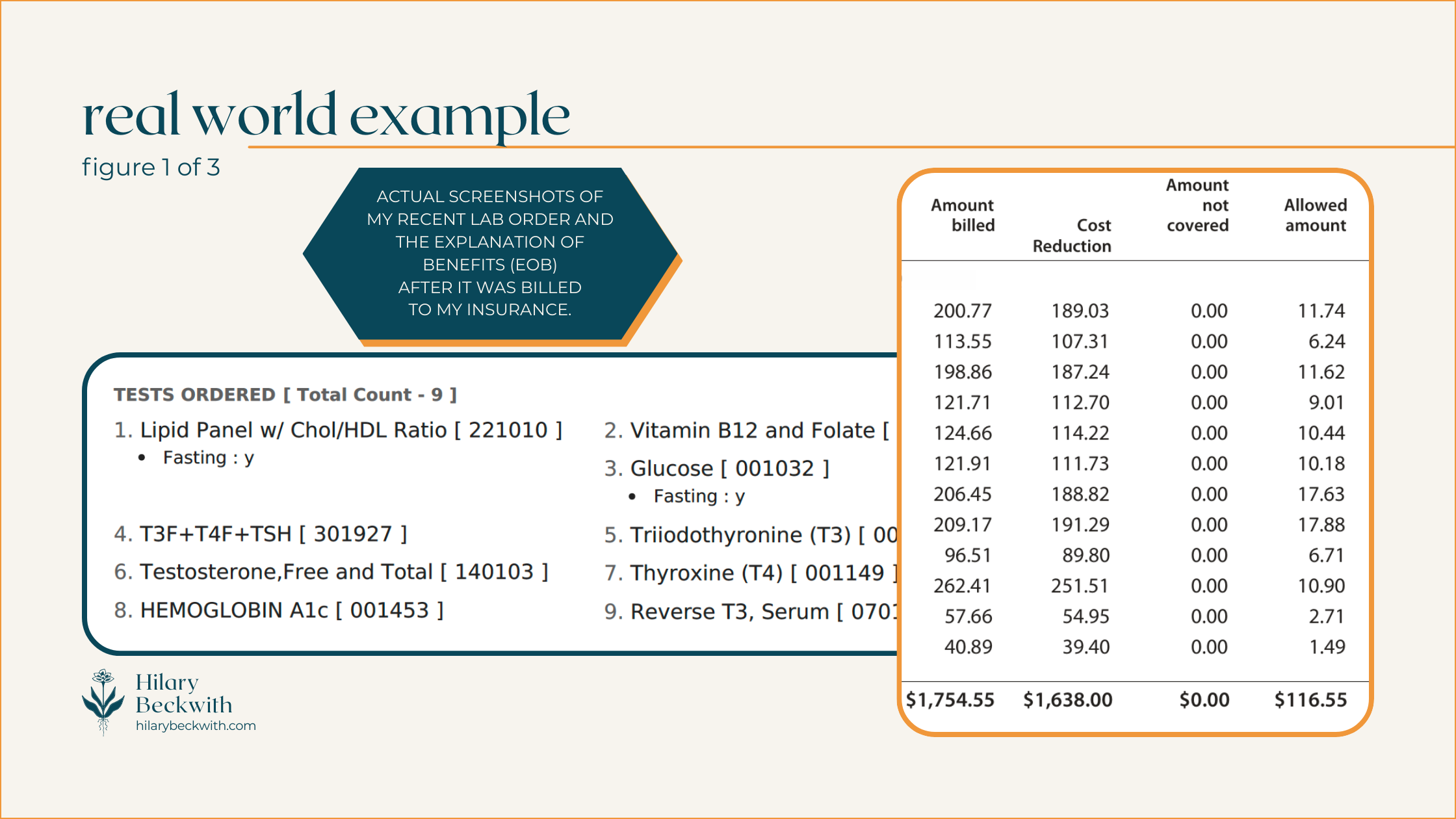

A common example of this is regarding thyroid testing. Many health insurance plans in the U.S. stipulate that in order to diagnose hypothyroid, TSH must be high, and free T4 must be low. Therefore, even if the patient has many other indications of hypothyroidism, your in-network practitioner will likely only test for TSH and fT4, unless you request otherwise.

Put more simply, health insurance plans are not designed to keep relatively healthy people, healthy. Health insurance plans are designed for symptoms-focused care and injuries.

Most health insurance plans do not cover services designed to optimize your health, such as functional lab testing, somatic work, treatments for complex trauma, and, yes, holistic nutrition consulting.

They’ll happily cover sleep medications, blood pressure medications, or weight loss surgery - but they will not cover the types of care needed to address root causes of insomnia, high blood pressure, and weight gain.

covered v. non-covered services

Health insurance is confusing - that’s why I’m here to bring some clarity to your world when navigating healthcare decisions, and those confusing EOBs.

I’ve included some diagrams below to help you understand things a bit better. But first, let’s talk vocabulary.

WHAT DO THESE COMMON HEALTH INSURANCE TERMS MEAN?

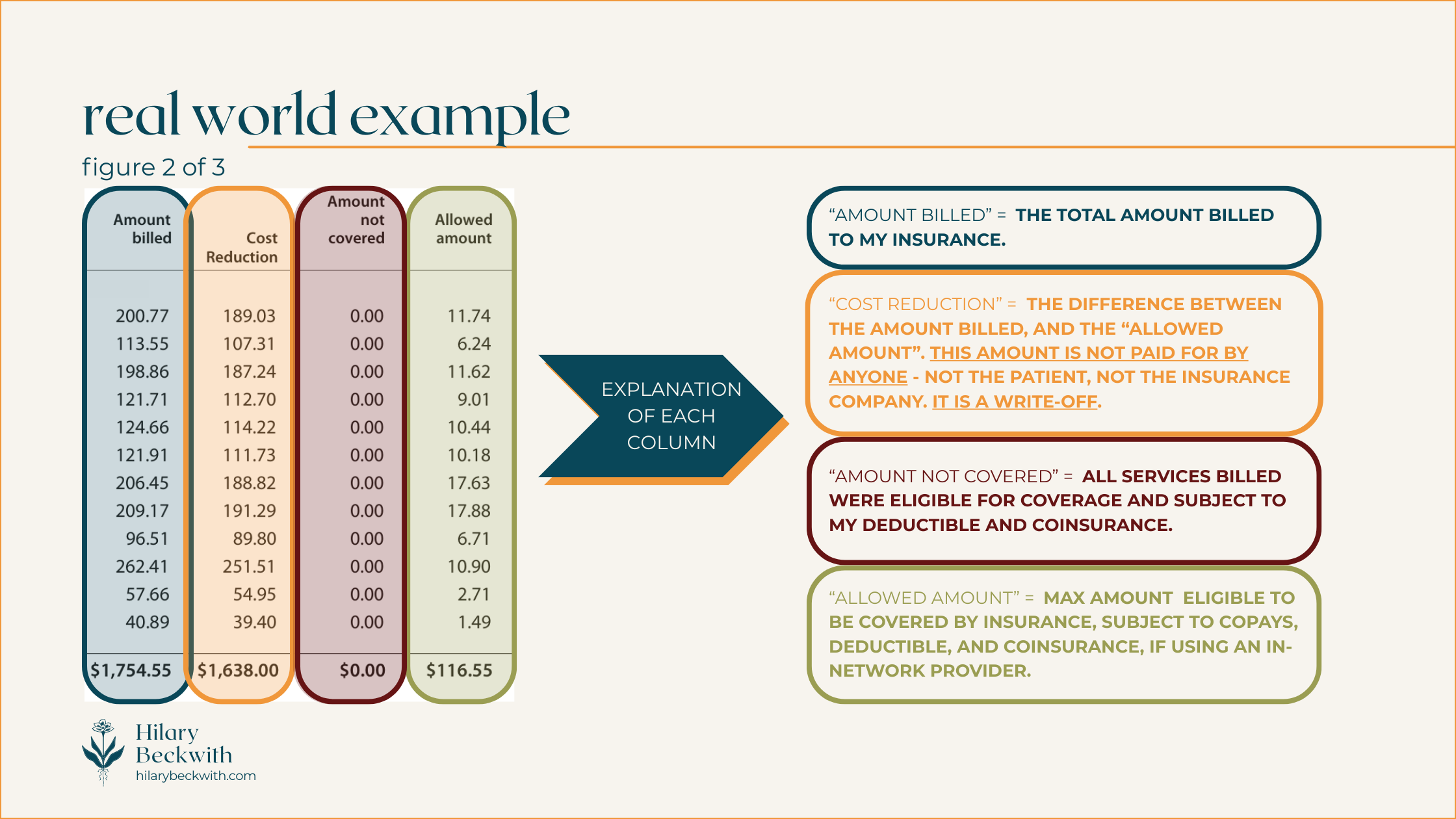

COVERED SERVICES:

A “covered” service is any service that is eligible for coverage, meaning it meets criteria set by the health insurance plan, including diagnosis, practitioner type, and plan inclusions.

A service that’s “covered” does not necessarily mean it is paid for by your insurance. A “covered” service is still subject to your plan benefits, such as deductible, coinsurance, or co-pay.

NON-COVERED SERVICES:

A “non-covered” service is any service that does not meet criteria set by the health insurance plan. The cost of a non-covered service is entirely the responsibility of the patient.

A service might be considered “non-covered” for the following reasons:

it is specifically excluded from your health insurance plan benefits

it was provided by an excluded practitioner type (e.g. a blood draw may not be covered if it is performed by a Naturopath if Naturopaths are excluded from your plan)

your diagnosis does not meet the requirements set by your insurance plan for the service to be covered - this does not mean your practitioner incorrectly diagnosed you.

the service was performed in a non-covered clinic or facility (e.g. getting Physical Therapy in a hospital setting may be covered differently than it would in an office setting).

IN NETWORK

Indicates a practitioner, facility, or group of practitioners, are contracted with a health insurance plan. As we discussed earlier, services from an in-network practitioner usually indicates “covered” service costs will be discounted.

OUT OF NETWORK

Indicates a practitioner, facility, or group of practitioners, are not contracted with a health insurance plan. Out-of-Network does not necessarily mean services will not be covered - but it does mean the costs will not be discounted.

DEDUCTIBLE

A dollar amount set by your health insurance plan, if applicable, that the patient must pay before the insurance begins paying for services. Coverage after the deductible is met varies from plan to plan.

EXAMPLE: If your insurance has a $1000 deductible, you must pay for services in full until they reach a total of $1000, after which your insurance will start paying according to your plan benefits. This only applies to “covered” services. Any non-covered services will not apply toward your deductible.

COINSURANCE

Not to be confused with a co-pay, a coinsurance is a percentage set by a health insurance plan that the patient is responsible to pay for all covered services. Most often, a plan that includes a coinsurance also includes a deductible, and similarly only applies to “covered” services.

EXAMPLE: If your insurance requires you to pay a 20% coinsurance, your insurance would pay 80% of covered services, and you would pay 20%. Typically this is applied after a deductible has been met.

CO-PAY

A co-pay is a flat-rate amount set by a health insurance plan that patient is responsible to pay for every eligible practitioner visit. Co-pay plans are very rare these days, and typically do not entail a deductible or coinsurance.

EXAMPLE: If your health insurance has a $30 co-pay, you would pay $30 when visiting a covered practitioner providing covered services, and insurance would pay for the rest. Some insurance plans may require separate co-pays for different types of services, even if they are provided by the same practitioner in the same day (e.g. a physical exam and a spinal manipulation may require two separate co-pays for the same visit)

do I take insurance?

Nope!

Or rather, it’s that insurance doesn’t take me.

As you’ve learned in this post, health insurance plans in the U.S. are more likely to cover treatments designed to suppress symptoms or change lab values.

It might even help you feel better for a time. But it won’t be the solution to your PCOS symptoms, IBS symptoms, weight gain, or anxiety. Those symptoms will all still be there the moment you stop taking the medications.

That’s why my work is focused on helping clients find and address root causes of their symptoms, not just changing lab values.

want to see what you’re missing?

learn something new?

Please share your thoughts and questions below.

NUTRITION SERVICES

ADDITIONAL RESOURCES

BLOG REFERENCES

Friedman, Jordan. “How Health Insurance Got Its Start in America.” History.Com, A&E Television Networks, 27 May 2025, www.history.com/articles/health-insurance-baylor-plan.